%20(2).png)

When Do You Plan To Retire?

- James

- Feb 3, 2025

- 3 min read

So, when do you plan to retire?

Have you given serious thought to this question?

When I ask this question to people, the answers typically fall into three categories:

Category 1: Between 60-65

Category 2: When I have enough

Category 3: A very specific age (usually 40 or below), along with a detailed plan of how they intend to get there.

If you're in the third category, I congratulate you and wish you the best of luck with your plan. If you fall in category 1 or 2, then this article is for you. If you’ve never heard of this before, I’ve linked a couple of articles here and here which may be of interest to you.

Category 1 or 2 responses allow people to push that decision many years down the road. The challenge is that by not thinking about it now, you risk failing to take the necessary steps today to ensure you get there. Especially those who have not defined what enough is.

Let’s say you have spent some time deciding on what age you plan to retire or defined how much is enough. The next big question is how will you fund your retirement. The standard answer people say here is my super will fund my retirement. But do you know how much is in your super, what fees are being paid or what your super is actually investing in? And the impact it could have over the long term? If you answered “I don’t know” to any of these questions then now is the time to start looking into this as it could have a dramatic impact on your future.

Here are a couple of examples to illustrate the point:

Example 1: Impact of fees

Age: 40

Current Value Of Super: $100,000

Average Predicted Annual Growth: 4%

Annual Contribution: $5000

Annual Fees: 0.5%

Planned Retirement Age: 65

The amount in your super would be $445,371. Not too bad, right? Well let’s look at the impact of just changing the fees from 0.5% to 2% and see what impact that would have over time.

Age: 40

Current Value Of Super: $100,000

Average Predicted Annual Growth: 4%

Annual Contribution: $5000

Annual Fees: 2%

Planned Retirement Age: 65

You would have $328,829. This is $116,542 less in your super and that was all down to how much you are paying in fees.

Imagine the impact that even higher fees could have on your Super. Hopefully this makes the point crystal clear.

Example 2: What is your super investing in?

Is your super invested in all international stocks or only domestic? How much of it is in cash or bonds? Are you comfortable with the company brands it’s invested in?

If you don’t know the answer to any of these questions, then it’s time to check the Product Disclosure Statement (PDS) of your super to find out what’s in there.

You can do this by Googling the name of your Super Company and the type of Super you have (which you should be able to find by logging into your online account).

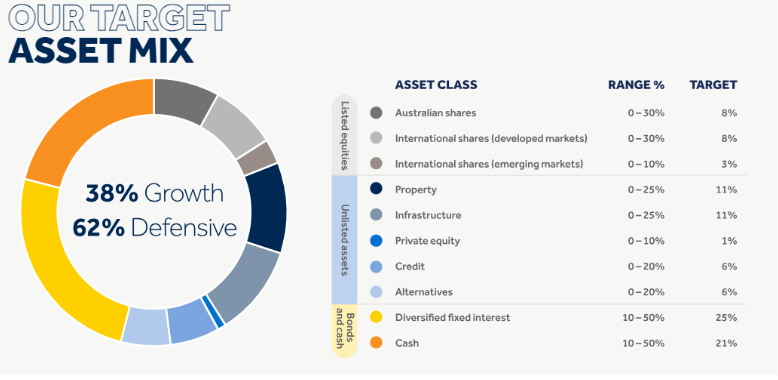

Here’s a couple of examples from HostPlus that highlight how different your allocation of Super could be. Note this is not an endorsement or recommendation, but a comparison of the few funds they offer.

High Growth Super Fund

Conservative Balanced:

Capital Stable:

As you can see their allocations are vastly different as they try to match their intended audience. Their allocation will also affect their long term performance. If you haven’t done so already, take a look at your own supers PDS to see how your funds are being allocated.

For those of you interested in learning more about investing, I offer a range of courses that can turn absolute beginners into Investment Pros. Get in touch to book your free 15 minute consultation.

Another big question when it comes to retirement is what are you going to do when you retire? Do you want to keep working but on your own schedule? Without the regular routine and purpose of a job, some people may feel a bit lost. The good news is, you can still claim your super and work if you choose. What about that hobby you never had time for? Well now you've got all the time in the world!

The intent of this post is not to give you all the answers but is a trigger for you to start seriously thinking about this topic and take action NOW before it’s too late.

Disclaimer: None of the content is intended to provide you with personal financial advice. Information provided is factual and educational in nature for you to apply at your own discretion. You may wish to seek independent financial advice from a professional advisor for advice pertaining to your specific situation.

Comments